ACA: Successes, Problems, Impacts

MCOL and Payers & Providers jointly sponsored a survey of healthcare professionals during April on healthcare industry expectations and attitudes regarding more significant provisions of the Affordable Care Act. An exclusive report on the survey findings follows.

Participants were asked to respond to four items:

-

Please categorize your organization.

-

Which of the following significant provisions of the Affordable Care Act do you feel has had the greatest degree of success thus far with regard to implementation and achieving its objectives?

-

Which of the following significant provisions of the Affordable Care Act do you feel has been the most problematic with respect to implementation and achieving its objectives?

-

Which of the following provisions of the Affordable Care Act do you feel will ultimately have the greatest impact on stakeholders?

Key Findings:

Overall, respondents are increasingly optimistic toward key Affordable Care Act provisions, particularly as they relate to implementation and achieving its objectives. According to the data, providers and vendors are primarily concerned with provisions concerning the formation of Health Insurance Marketplaces; while payers are primarily concerned with provisions concerning guaranteed health insurance.

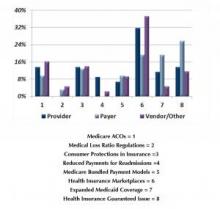

Medicare Accountable Care Organizations

Key findings with respect to the Medicare ACOs provision indicate that 20.5% of providers and 23.3% of vendors surveyed believe that this provision has had the greatest degree of success thus far with regard to implementation and achieving its objectives. Conversely, a relatively low percentage of payers surveyed (3.2%) believe that this provision has had the greatest degree of success thus far when asked the same question.

However, despite the plurality concerning the success of implementing Medicare ACOs, there is apparently less consensus with respect to how problematic it has been.

According to the data, 25% of providers, 3.2% of payers, and 9.3% of vendors surveyed view the implementation of Medicare ACOs provisions as problematic.

Finally, when asked which provisions will ultimately have the greatest impact on stakeholders; only 13.6% of providers, 9.7% of payers, and 16.3% of vendors identified the Medicare ACOs provisions

Health Plan Medical Loss Ratio Regulations

Key findings with respect to the health plan medical loss ratio (MLR) Regulations provision indicate that 22.6% of payers and 20.9% of vendors surveyed believe that the provision has had the greatest degree of success thus far with regard to implementation and achieving its objectives.

On the other hand, only 11.4% of providers surveyed (3.2%) believe that this provision has had the greatest degree of success thus far when asked the same question.

Once again, despite the plurality concerning the success of implementing the MLR regulations provision, there is disagreement with respect to how problematic it has been. In this case, 2.3% of providers, 12.9% of payers, and 9.3% of vendors surveyed view the implementation of MLR provision as problematic.

However, only 4.7% of vendors and 3.2% of payers surveyed expect that MLR provision will ultimately have the greatest impact on stakeholders. Perhaps unexpectedly, no provider respondents surveyed expect that MLR provision will ultimately have the greatest impact on stakeholders.

Consumer Protections In Health Insurance

(Applicable restrictions on lifetime limits, rescinding coverage, pre-existing medical conditions, annual limits)

Key findings with respect to the consumer protection provisions indicate that this is the greatest concern for all three constituent groups surveyed. In fact, 54.5% of providers, 51.6% of payers, and 44.2% of vendors surveyed believe that these provisions have had the greatest degree of success thus far with regard to implementation and achieving its objectives.

In accordance with the perceived success of implementing the consumer protection provisions, only 2.3% of providers, 9.7% of payers, and 11.6% of vendors surveyed found the implementation of consumer protection provisions problematic.

Of those surveyed, 13.6% of providers, 12.9% of payers, and 14.0% of vendors expect that the consumer protection provisions will ultimately have the greatest impact on stakeholders.

Reduced Medicare Payments For Hospital Readmissions

Key findings with respect to the reduced Medicare payments for hospital readmissions provision indicate that 6.8% of providers, 19.4% of payers, and 9.3% of vendors surveyed believe that this provision has had the greatest degree of success thus far with regard to implementation and achieving its objectives.

At the same time, 11.4% of providers, 16.1% of payers, and 9.3% of vendors surveyed view the implementation of this provision as problematic.

As expected, 9.1% of providers and 2.3% of vendors surveyed expect that the Hospital Readmissions provisions will ultimately have the greatest impact on stakeholders. Perhaps unexpectedly, no payers surveyed identified these provisions as ultimately having the greatest impact on stakeholders.

Medicare Payment Bundled Payment Models

Key findings with respect to the Medicare bundled payment model provisions indicate that 6.8% of providers, 3.2% of payers, and 2.3% of vendors surveyed believe that these provisions have had the greatest degree of success thus far with regard to implementation and achieving its objectives.

Concurrently, 15.9% of providers and 4.7% of vendors surveyed view the implementation of bundled payment model provisions as problematic. As expected, no payers identified this as problematic.

Moreover, 6.8% of providers, 9.7% of payers, and 9.3% of vendors surveyed expect that the bundled payment model provisions will ultimately have the greatest impact on stakeholders.

Health Insurance Marketplaces

Key findings with respect to the health insurance marketplaces (HIX) provisions indicate that 20.5% of providers, 38.7% of payers, and 37.2% of vendors surveyed believe that these provisions have been the most problematic thus far with regard to implementation and achieving its objectives.

Overwhelmingly, 31.8% of providers, 19.4% of payers, and 37.2% of vendors surveyed expect that the HIX provisions will ultimately have the greatest impact on stakeholders.

Expanded Medicaid Coverage

Key findings with respect to the expanded Medicaid coverage provisions indicate that similarly to attitudes regarding the Health Insurance Exchange provisions; 22.7% of providers, 19.4% of payers, and 18.6% of vendors surveyed believe that the Expanded Medicaid provisions have been the most problematic thus far with regard to implementation and achieving its objectives.

Furthermore, 11.4% of providers, 19.4% of payers, and 4.7% of vendors surveyed expect that the expanded medicaid provisions will ultimately have the greatest impact on stakeholders.

Health Insurance Guaranteed Issue/Elimination of Pre-Existing Conditions

Key findings with respect to the Guaranteed Issue provisions indicate that 13.6% of providers, 25.8% of payers, and 11.6% of vendors surveyed expect that the Guaranteed Issue provisions will ultimately have the greatest impact on stakeholders.